SB 254 Catastrophe Resiliency study emphasizes need for new wildfire mitigation financing strategies

California’s escalating wildfire crisis poses multiple serious risks to the state. Recognizing the need for new approaches, the Legislature and Governor authorized a Catastrophe Resiliency study – the ‘SB 254 Report’ – to evaluate policy options to reduce damages to life and property, accelerate post-disaster recovery, and improve the allocation of wildfire-related costs in California.

In this blog, we summarize the report’s main recommendations – which span a range of potential actions including targeted fixes, such as strengthening community-level capacity and expediting project environmental review, to more transformational changes, such as reforming inverse condemnation and establishing new state-coordinated financing strategies that mobilize a blend of public and private capital for wildfire mitigation.

We then consider near-term opportunities to implement priority recommendations, including new strategies to finance wildfire mitigation. We highlight two bills – SB 1297 (Allen) and AB 1666 (Rogers) – that closely align with the report’s recommendations.

A central message of the SB 254 Report is that California’s current system for managing wildfire is no longer fit for purpose given the scale of the risk. As a result, inaction is the worst possible outcome. By adopting a portfolio of recommended actions, the state can get on a path to address some of its most important challenges, including energy affordability, insurance availability, and public health and safety in the era of climate change.

* * *

Wildfires pose multiple key risks to California – including the uninsurability of large swathes of the state, utility bankruptcies, grid failures, megaton-scale greenhouse gas emission events, and the loss of life and property. The LA fires alone caused hundreds of billions of dollars in damages to infrastructure and public health. The costs of investor-owned utility wildfire mitigation are by far the primary driver of the state’s high electricity costs.

As part of last year’s climate and affordability bill package, the Legislature and Governor authorized a Catastrophe Resiliency study – the ‘SB 254 Report’ – to evaluate options for how to manage wildfire prevention, liability, recovery, and cost-sharing going forward. In this blog, we summarize the report’s main findings before highlighting near-term opportunities to implement priority recommendations.

SB 254 Report scope and goals

SB 254 (Becker, Petrie-Norris) authorized the California Earthquake Authority (CEA) to develop a report that “evaluates and sets forth recommendations on new models or approaches that mitigate damage, accelerate recovery, and responsibly and equitably allocate the burdens from natural catastrophes, including catastrophic wildfires.”

The motivation for this mandate followed the LA wildfires in January 2025 – the magnitude of which would largely deplete the state’s $21 billion Wildfire Fund. The reality that a single catastrophic event could undermine what was widely considered to be a fairly robust backstop policy underscored the need to look towards new and more durable models for wildfire resilience in California.

SB 254 provided key guidance for the CEA’s recommendations, including to examine key issues including insurance markets, utility liability, claims processes and post-disaster recovery, community planning, project financing, and more – highlighting the sheer complexity and interconnected nature of the problem. The report established three leading goals, including to ensure:

#1: Affordable, safe, reliable, and clean energy, provided by stable utilities able to meet long-range climate and energy goals;

#2: Access to a robust, competitive, and fairly regulated property insurance market able to meet the recovery promise for all policyholders; and

#3: Safe, catastrophe-resilient communities.

Context: California’s catastrophe loss problem

Before summarizing the recommended actions, it is notable that the report places emphasis on the cost of inaction. That is – although there are both near-term and long-term costs associated with taking action to improve wildfire resilience in California, the costs of not making these changes are considered significantly higher.

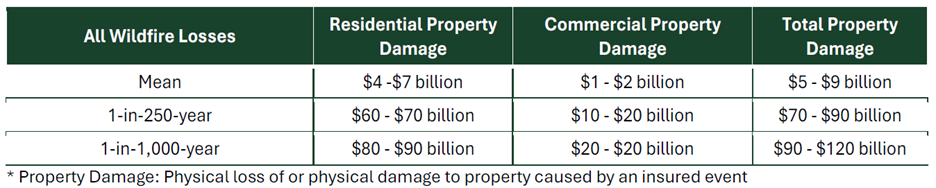

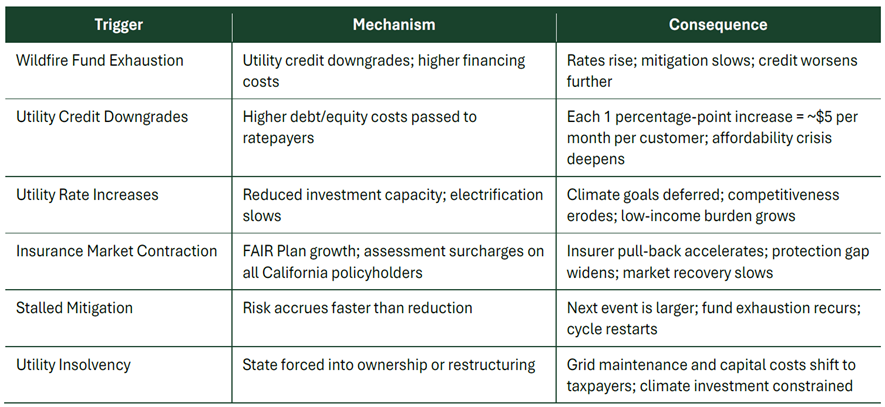

Figures 1 and 2 provided further information on this point:

Figure 1 shows how a 1-in-250-year event is estimated to cost up to $90 billion in property damages. This excludes the broader public health impacts, which could easily double this estimate. A key takeaway here is that upfront investments to avoid or significantly mitigate just one of these events over the coming decades would be worthwhile.

Figure 2 summarizes the systemic nature of the problem, including the cascading consequences that ratepayers, homeowners, and communities remain exposed to in the absence of action to improve the state’s wildfire resilience.

Figure 1: Estimate of damages to property under different levels of wildfire severity. Source: SB 254 Report

Figure 2: Summary of consequences from inaction on wildfire resilience. Source: SB 254 Report

Key recommendations

After establishing the study mandate and goals as well as a baseline of what to expect in the case of inaction, the report identifies a suite of potential actions – ranging from targeted policy fixes to transformational changes that address key institutional limitations.

The report identifies three overarching Policy Pathways, each of which are comprised of multiple strategies and actions. We summarize each of these in turn.

Pathway 1: Commit to community wildfire risk reduction

Summary: This pathway primarily focuses on strengthening existing community mitigation programs, including with greater state coordination, guidance, and resources for local governments, increased capacity at the community level, developing shared data and information to support local mitigation planning, and setting some new requirements that further support existing priorities related to electric utility safety, accountability, and reporting.

Strategy #1: Enhance the statewide approach to driving targeted community wildfire risk reduction, such as via developing data and analytical resources, adopting science-based standards for home mitigation (e.g. Zone Zero requirements), and streamlining project review processes.

Strategy #2: Stimulate community- and home-level commitment and responsibility for wildfire resiliency, including via incentives for community mitigation planning and pre-disaster recovery and via tightening the link between risk reduction and insurance.

Strategy #3: Continuing to prioritize electric utility safety and accountability, such as via preserving certain existing standards and developing new base requirements related to risk tolerance and tying executive compensation to safety outcomes.

Pathway 2: Equitably allocate catastrophe burdens

Summary: This pathway focuses on addressing the fundamental problem that existing cost-sharing structures are not fit-for-purpose to manage the extreme wildfires we are now experiencing in California. This includes issues such as investor-owned utilities being burdened with inverse condemnation, residential ratepayer making disproportionate contributions to wildfire mitigation, multiple homeowners being unable to purchase property insurance, and the relatively slow speed of post-disaster compensation payments.

Strategy #1: Strengthen access to residential property insurance for homeowners and renters, such as via FAIR Plan reform, enhanced market oversight and monitoring, and solidifying the Sustainable Insurance Strategy.

Strategy #2: Reform utility liability, including via eliminating or modifying inverse condemnation rules as well as eliminating insurance subrogation.

Strategy #3: Accelerating recovery compensation payments and reducing legal costs, including via a new "fast pay" facility for survivors of utility-caused wildfires.

Strategy #4: Make a more durable, permanent Wildfire Fund, such as via various forms of risk transfer from ratepayers and more diversified funding sources (e.g., state, county, municipal, and other private sources. such as from insurance and reinsurance markets).

Pathway 3: State roles for addressing catastrophe resiliency

Summary: This pathway focuses on financing strategies to improve wildfire resilience including via two avenues. First, and following Pathway 2, is that even if we address key issues in the system today, there is still fragility to catastrophic events. This pathway therefore highlights additional, state-coordinated mechanisms to address this residual burden. Second, this pathway highlights the need for new public and private financing strategies to facilitate wildfire mitigation, such as home and community hardening, defensible space, and vegetation management. The state cannot achieve wildfire resilience without implementing these on-the-ground actions.

Strategy #1: State roles to finance catastrophe risk, such as via establishing a state wildfire liability insurance program for utilities, a state backstop for electric utility wildfire liability, and a state-backed catastrophe reinsurance layer for the residential property insurance market.

Strategy #2: Statewide funding for community wildfire mitigation, such as via state-coordinated financing models that blend public revenue, private investments, and bioeconomy development, in coordination with a variety of financing tools such as low-cost loans, loan guarantees, bond issuances, credit enhancements, and similar strategies.

Implementation opportunities

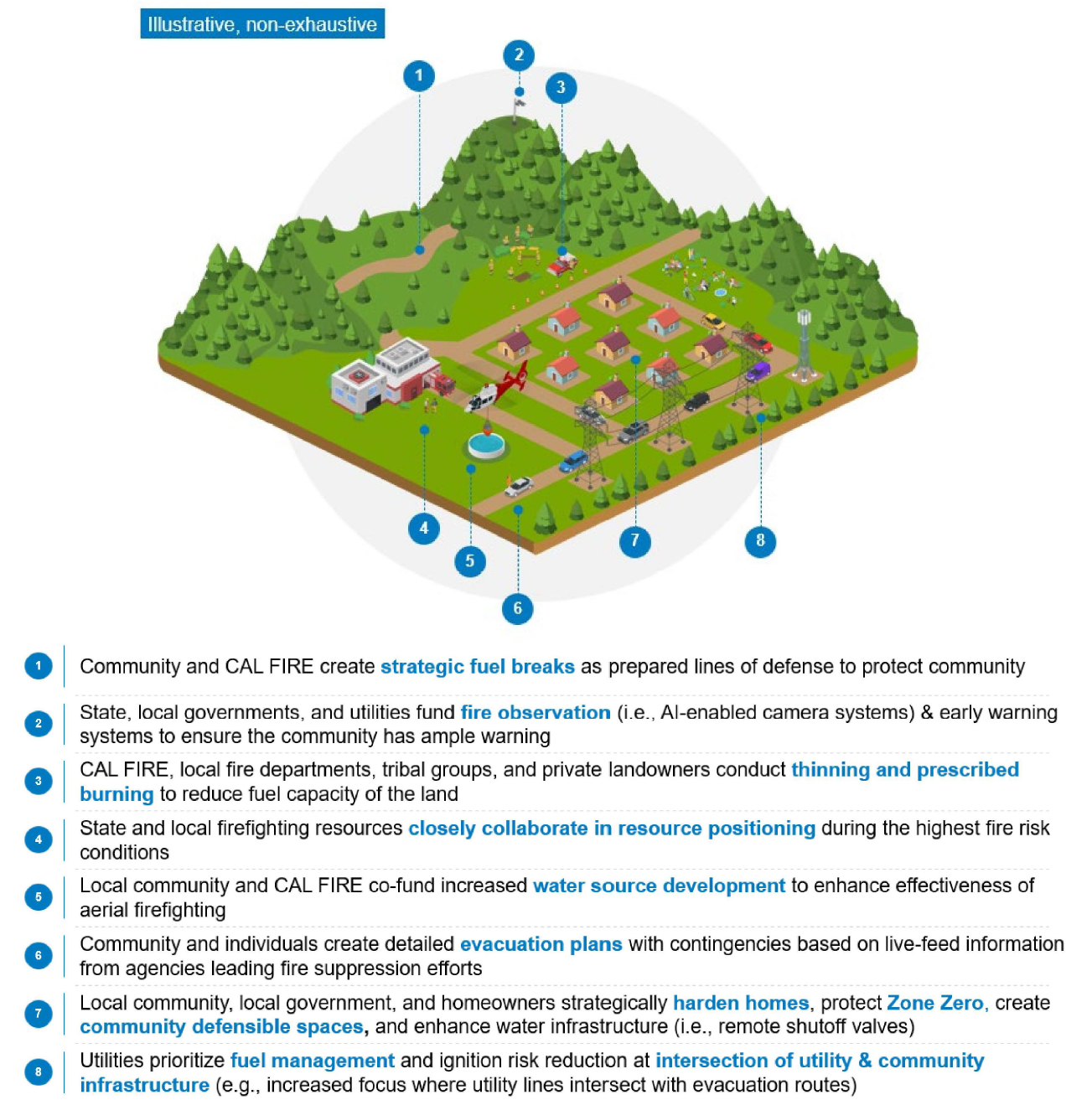

A key theme and takeaway from the SB 254 Report – one which underlies multiple recommended actions – is that the only way the state can achieve durable wildfire resilience is to increase wildfire mitigation via actions including home and community hardening, defensible space, and landscape-scale vegetation management. Figure 3, from the investor-owned utilities submission to the SB 254 Report process, nicely illustrates the combination of actions needed to achieve community wildfire mitigation.

Figure 3: Summary of actions to achieve community wildfire mitigation. Source: IOUs submission

In a previous analysis, we highlighted the main obstacle to increasing wildfire mitigation in California: a lack of available funding. There is simply not enough resources across state and federal budgets to come close to delivering the state’s wildfire mitigation goals. This same conclusion is reached in the report – which dedicates an entire section to exploring new mechanisms to support wildfire mitigation financing. The report highlights a key role for the state to stand-up and coordinate these new mechanisms:

“A coordinated financing model – blending public revenue, private investment, and bioeconomy development – has the potential to stretch limited local, State and Federal dollars.”

It is notable that two current bills before the Legislature – SB 1297 (Allen) and AB 1666 (Rogers) – could serve to substantively implement the set of wildfire mitigation financing recommendations identified in the SB 254 Report. We briefly summarize each of these bills, below.

SB 1297 (Allen) – Regional Wildfire Mitigation Public-Private Partnerships

SB 1297 would establish a new mechanism to mobilize both public and private capital for wildfire mitigation. Specifically, it would incentivize regional public-private partnerships, including public agencies, utilities, insurers, and potentially other non-profit or private entities, to determine their respective financial benefits from implementing regional mitigation plans. As an example, this could include the value of liability risk reduction on the part of utilities and insurers--and specifically a determination of what those entities would be willing to pay ($) to realize that benefit. This 'revenue stack' would be memorialized in a contract and could support a bond issuance, including by the California IBank, to provide upfront capital in support of priority mitigation projects.

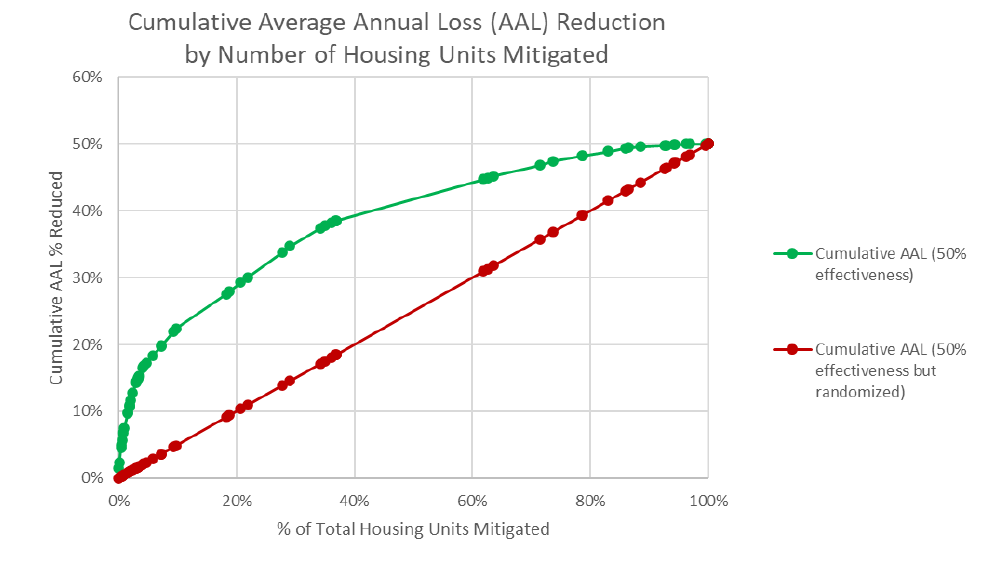

Importantly, this financing method – known as 'pay for success' – has been successfully applied to drive conservation investments globally, but also in California. This mechanism could support rapid and targeted investments in high-risk communities, which the report shows could have a disproportionate benefit in terms of loss reduction (Figure 4).

Figure 4: Shows how average losses from home mitigation are substantially reduced as part of a coordinated regional strategy (green) vs. uncoordinated or randomized strategy (red). Significant gains can be achieved for the first 10% of homes mitigated. Source: SB 254 Report

AB 1666 (Rogers) - Biomass Innovation Parks

AB 1666 would facilitate the expansion of a sustainable forest bioeconomy in California and in doing so support the cost of forest treatments. Specifically, the bill would allocate funding from Proposition 4 to support the development of one or more Biomass Innovation Parks to support the development and scale-up of clean, non-combustion technologies identified by the California Air Resources Board as needed to achieve the state’s climate goals. Additionally, the bill would address other key obstacles, such as the inability to access long-term feedstock supply from federal lands, as well as establish key tools to support supply chains, such as mechanisms to trace and authentic forest biomass origins.

Compared to SB 1279, which focuses more on the wildland-urban interface and urban areas, AB 1666 would support wildfire mitigation in forested landscapes. Additionally, it would deliver a host of co-benefits, including rural and tribal economic development, air quality improvements from avoided pile burning, and significant emissions reductions. Figure 5 provides a broad summary of technology options and processing pathways, including innovative wood products, clean fuels, and carbon dioxide removal.

Figure 5: Non-exhaustive summary of non-combustion technology options consistent with CARB's Scoping Plan. This diagram is illustrative only--for example, it should be noted that municipal solid waste (MSW) is outside the scope of AB 1666. Source: World Resources Institute

Conclusion

California is at a critical juncture on wildfire. The SB 254 Report provides a comprehensive assessment of options to improve outcomes in terms of energy affordability, property insurance, and public health and safety. The report identifies three broad Policy Pathways that would serve to: (i) strengthen existing community programs; (ii) reform cost-sharing across stakeholders to reflect the 'new normal' of severe wildfire in California; and (iii) establish new state-coordinated financing tools to further reduce downside risk as well as facilitate an increase in the pace and scale of community wildfire mitigation.

The key, though, is seeing a portfolio of these recommendations through to implementation. This article highlighted two current bills, SB 1297 (Allen) and AB 1666 (Rogers), that could serve to substantively implement the set of recommendations related to wildfire mitigation financing. For more information, please contact Sam Uden (sam@netzerocalifornia.org).