GGRF investments are a dumpster fire. Does anyone even care?

The cap-and-invest program update has quickly become one of the most contentious environmental policy fights of 2026.

The California Air Resources Board’s (CARB's) proposal to establish a Manufacturing Decarbonization Incentive (“MDI”) that would reduce near-term compliance costs for manufacturers, notably refineries, has been strongly opposed by environmental organizations. Industry groups, meanwhile, have argued it doesn’t go far enough in addressing leakage risks. The Legislature has expressed deep frustration over how the MDI could significantly reduce Greenhouse Gas Reduction Fund (GGRF) revenues and therefore undermine the spending commitments agreed under SB 840 (Limon). The budget chairs in both houses have suggested reopening these negotiations.

With gas prices exceeding $6 per gallon and no federal support on climate issues, CARB is in a difficult position – and indeed much of the debate has treated this moment as a series of unfortunate geopolitical and economic events.

But California has been vulnerable to this moment for years. The state has spent more than a decade generating tens of billions in GGRF revenues without deploying those funds in ways that complement a tightening cap. Carbon pricing has key limitations – it creates pressure to decarbonize at the margin, but does little to drive innovation in new technologies or support the development of large-scale climate infrastructure. If California had been deploying GGRF more strategically toward these broader energy transition needs, there is a good chance that the compromise package now headed to CARB members would have been less controversial – and perhaps not needed at all.

The Legislature has the ability to remedy this issue – although at this stage lawmakers have indicated that the existing allocations remain a priority. In this blog, we remind stakeholders of how horrendously underperforming the current portfolio of GGRF investments are for the purpose of emissions reductions. We highlight one of the few bright spots from SB 840 – which was the $85M allocation to support climate-focused technological innovation. We suggest that ramping-up this investment is a key opportunity, as is capitalizing a new infrastructure fund to address deployment barriers for emerging clean industries.

It is imperative that CARB approve the proposed program update without delay so as to avoid any further uncertainty for market participants. By pairing this with structural GGRF reform, policymakers can turn a difficult moment into a meaningful course-correction. Without it, both the state’s climate goals and the long-term integrity of the cap-and-invest program will remain at risk.

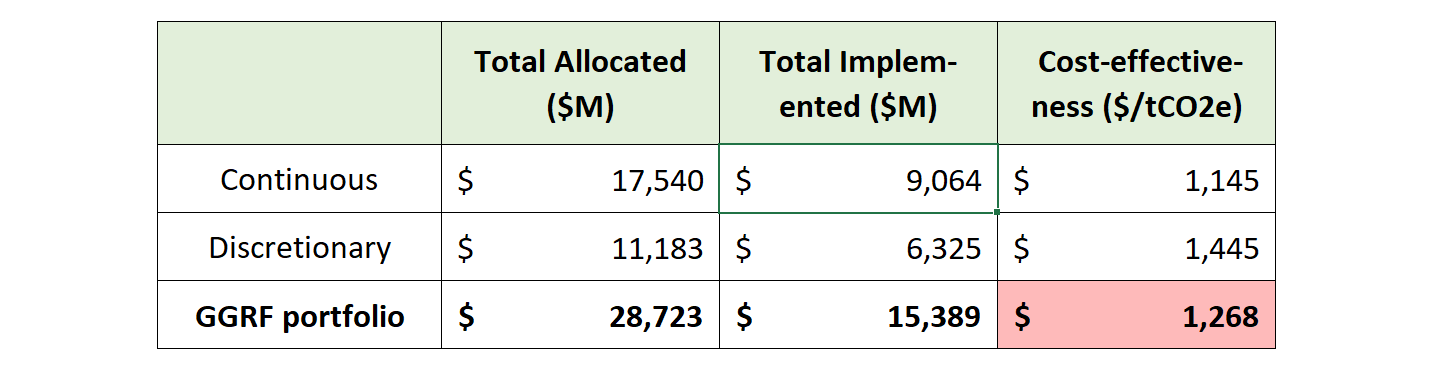

Fact #1: The GGRF portfolio is wildly cost-ineffective

The GGRF portfolio is split into two main categories: continuous and discretionary allocations. Continuous allocations support core GGRF programs including high-speed rail, affordable housing and sustainable communities, and transit, and receive roughly 60-65% of total revenues ($17.5B since 2014). Discretionary allocations support roughly 80 programs that are liable to change in a given year, but the main areas funded to date include various low-carbon transportation, forest health, and air quality programs. Discretionary programs receive the remaining revenues ($11.2B since 2014).

Both the continuous and discretionary GGRF portfolios are grossly underperforming in terms of cost-effectiveness, with programs across both categories routinely providing zero emissions reductions or requiring thousands of dollars to reduce one ton of carbon emissions. Based upon publicly available data, the weighted average cost-effectiveness of 90 GGRF programs is $1,268/ton (Table 1). By rough comparison, the most recent cap-and-invest auction clearing price was $28/ton. This means it costs GGRF 45x more than what it takes to reduce a ton of carbon emissions in a competitive market.

Table 1: Weighted average cost-effectiveness of GGRF portfolio. Note: These estimates are based upon 2024 CCI data, as 2025 data does not readily provide certain estimates, such as "Total Allocated ($M)". Although, it is clear that the $/ton estimate of the 2025 data is consistent with this estimate and greater than $1,000/ton. For more information, see Data analysis of cap-and-invest program investments (April 2025).

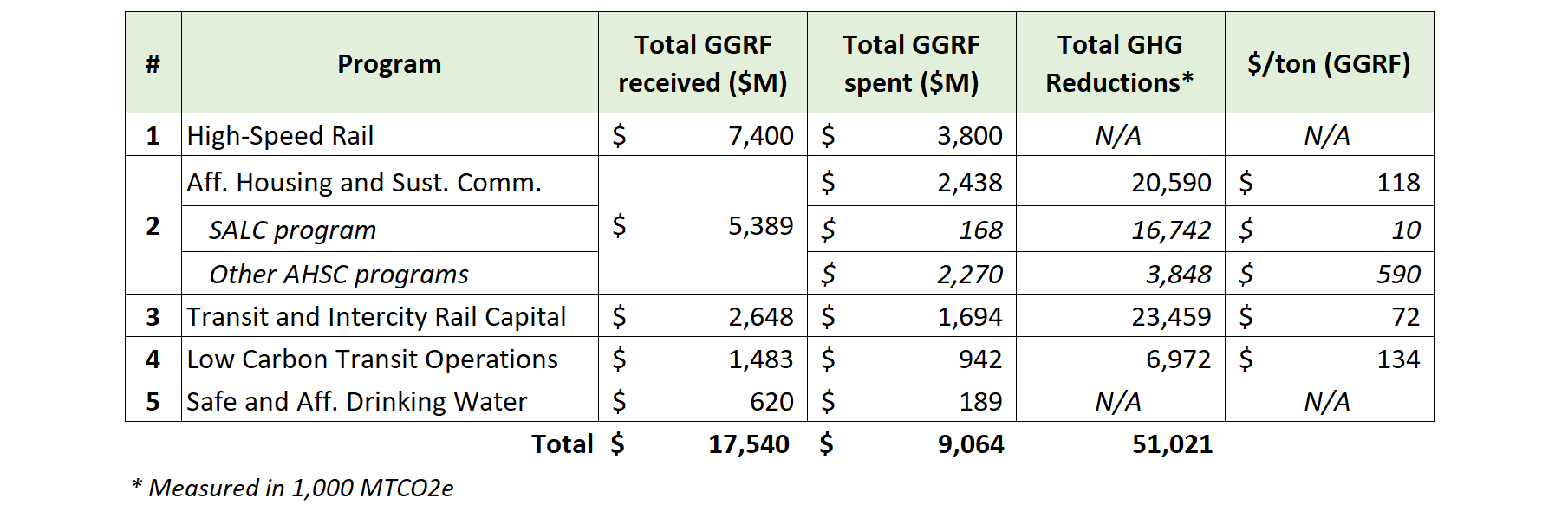

Fact #2: GGRF investments bear almost no relation to the 2022 Scoping Plan

Cost is important – but it is not the only thing that matters. It makes sense that in many cases GGRF would be spent on higher cost actions or technologies, given these aren't incentivized by a relatively low carbon price under a cap-and-invest program. What matters, though, is that these actions or technologies are the things we have identified as needed to achieve our climate goals.

Unfortunately, there is a substantial misalignment between current GGRF spending and the 2022 Scoping Plan, which did not identify core programs including high-speed rail, affordable housing and sustainable communities, or transit programs, as priority investments for achieving the state’s net-zero emissions by 2045 goal. These allocations were established more than a decade ago in 2014, and have been unchanged ever since. At that point, California did not even have a 2030 climate goal, let alone a net-zero goal. 100% clean energy was not a target. The Paris Agreement wasn’t even signed.

These continuous allocations exhibit a cost-effectiveness $/ton range from “N/A” (i.e., zero emissions reductions to date) to $590/ton (Table 2), but there are multiple key details to consider:

High-Speed Rail (HSR): Although HSR provides no emissions reductions, if the project can achieve its forecast reductions (160,000 tCO2) by 2030 this would yield a $/ton estimate of about $84,000/ton.[1] If HSR is implemented according to its medium total project cost estimate ($106B) and continues to receive GGRF at a similar level to today, by 2045 it could achieve between $819/ton to $3,780/ton.[2]

Affordable Housing and Sustainable Communities (AHSC): AHSC is reported as having an overall cost-effectiveness of $118/ton. However, the data shows that the Sustainable Agricultural Lands Conservation (SALC) program, which is one of five programs that make-up the AHSC portfolio, drives the majority of the benefits. If removed, AHSC cost-effectiveness increases to $590/ton.

Transit and Intercity Rail Capital: The Transit and Intercity Rail Capital program has implemented 245 projects, generating 23 million tons of emissions reductions at $72/ton. However, it should be noted that 20 projects (8%) provide 70% of the emissions reductions. 6 projects (2%) provide 50% of the emissions reductions. These projects primarily include BART and LA Metro investments.[3]

Table 2: Continuous allocation program performance. Source: Data analysis of C&I program investments.

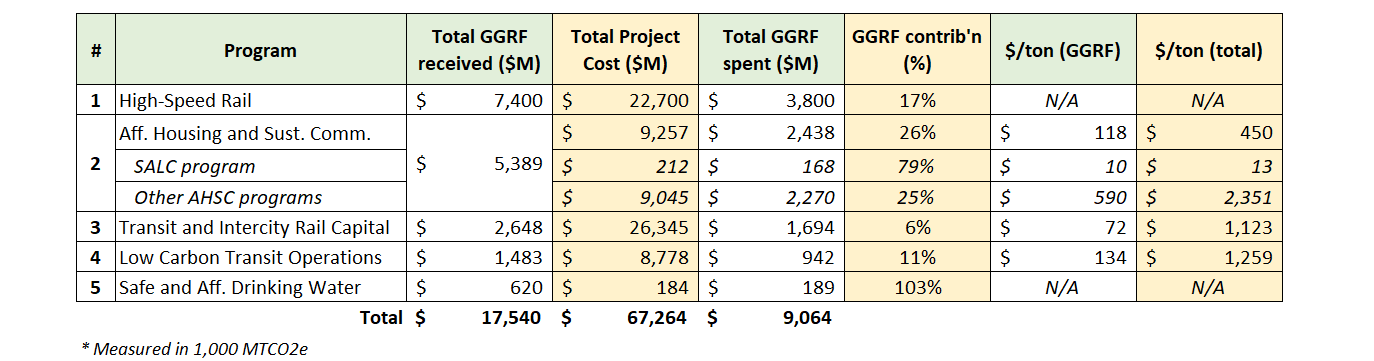

Fact #3: GGRF investments as a portion of total project costs increase the cause for concern

Despite GGRF data already leaving a lot to be desired, it is notable that the above $/ton estimates arguably overstate performance. This is because total project emissions reductions are credited to the GGRF investment, while GGRF generally only contributes a portion of total project costs. For example, the SALC program has implemented $168 million in GGRF funds, but total project costs are $212 million (i.e., GGRF provided 79% of total funding – which is an example on the higher end).

It is possible to calculate an alternate measure of cost-effectiveness based upon total project costs. As expected, a total project cost benchmark shows a reduction in cost-effectiveness (Table 3). For example, AHSC programs see a $/ton increase from $590 to $2,351, while Transit and Intercity Rail Capital increases from $72 to $1,123 – both owing to substantial non-GGRF project costs. An argument could be made that, as projects would not have proceeded without GGRF, it is reasonable to count the total project emissions reductions. However, this argument may not hold to the extent GGRF accounts for a relatively minor (e.g. less than 10% or 20%) share of total project costs.

Table 3: GGRF vs. total project costs. Data shows that transit and high-speed rail programs are not heavily dependent on GGRF as a portion of total project costs. In contrast, safe drinking water would likely not exist without GGRF. Source: Data analysis of C&I program investments.

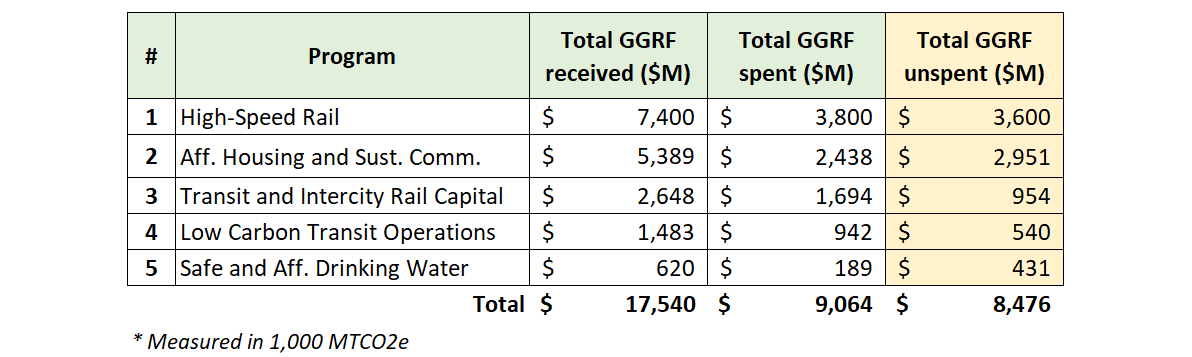

Fact #4: GGRF programs are sitting on billions in unspent funds

A key challenge – should state leaders be interested to reallocate GGRF to align with the state's climate goals – includes how to transition the current set of appropriations to this new investment strategy. Short of providing a recommendation, we simply note that current continuous programs all maintain hundreds of millions or billions of dollars in unspent funds (Table 4). This is one data point that suggests a more rapid phase down of funding may be acceptable. Consultation with the relevant agencies is important to understand their planned projects as well as to develop a credible phase-down and transition strategy.

Table 4: Summary of GGRF unspent funds. Source: Data analysis of C&I program investments.

How GGRF could be catalytic for the state's climate goals

Cap-and-invest is a key pillar of the state’s climate policy portfolio, but it faces two important limitations that – by design – should be resolved with a targeted allocation of GGRF revenues.

High-cost, innovative technologies

First, a low carbon price does little to incentivize the development of high-cost technologies identified as needed to meet the state’s climate goals. In the 2022 Scoping Plan, CARB identified a number of clean technologies with costs well in excess of $100/ton, including industrial decarbonization ($200+) and carbon removal ($700+) (Table 3-11, p. 155). The current cap-and-invest clearing price of $28/ton is far too low to incentivize developers to buy-down these technology costs. GGRF should be deployed to support this research, development and demonstration and push these zero-carbon solutions to become available "under the cap". The $85M for climate-focused technology innovation, as identified in SB 840, is a bright spot from last year's negotiations – and should be substantially increased.

Large-scale climate infrastructure

Second, a low carbon price does little to incentivize large-scale climate infrastructure, particularly for new industries such as clean fuels and carbon management – which require coordinating multiple distinct projects including pipelines and storage complexes. For example, even with a very high $150/ton carbon price that may on paper justify a cement facility in investing in a carbon capture retrofit, the facility owner won't make this investment decision unless there is a pipeline available to offtake the CO2. The same is true for heavy-duty electric vehicles that need a sufficient charging infrastructure network, clean fuels such as hydrogen and RNG that may need pipelines and storage, and others. GGRF could be deployed to support these chicken-or-egg problems by capitalizing a fund that provides low-cost loans to de-risk and enable commercialization of key climate infrastructure.

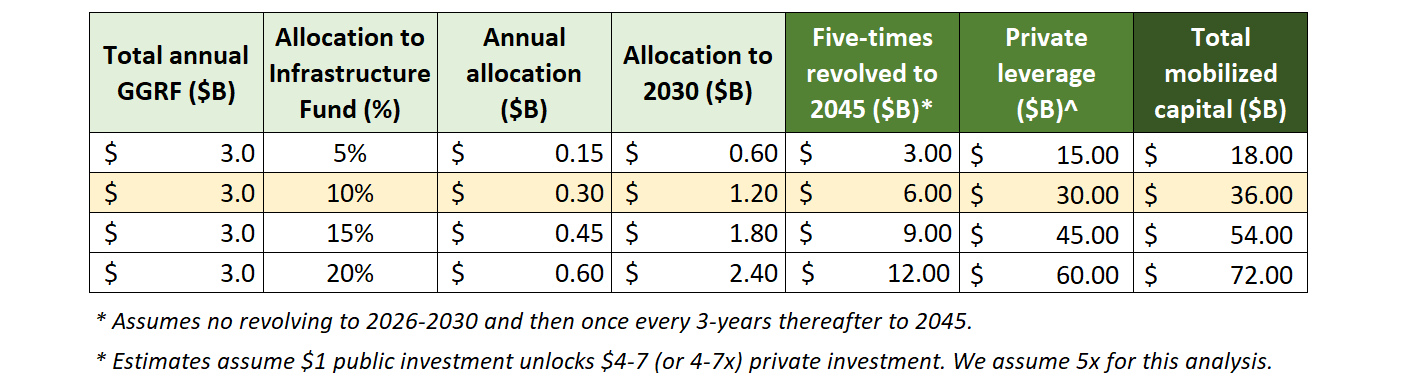

We provide an example of how an infrastructure fund could work in practice (Table 5). If $1.2B of GGRF ($300M/yr for four-years) was used to capitalize a revolving fund that provides loans that are repaid and redeployed every few years, this could total $6B in public investments by 2045. Assuming this leverages private capital (mid-range estimate of 5x), this would generate $36B in total mobilized capital.

Table 5: Capitalizing a revolving climate infrastructure fund could substantially multiply the climate benefits of the GGRF portfolio. For example, allocating $300M per year from GGRF could total $1.2B in 2030, which if revolved on a conservative schedule could mobilize $36 billion in total public and private capital by 2045.

Conclusion

California has appropriated over $30 billion dollars in GGRF investments to programs and projects that in many cases provide little, if any, climate benefits. Even with the proposed Manufacturing Decarbonization Incentive, roughly $10 billion more could be generated this side of 2030. Imagine if this funding was deployed strategically and in support of the state's climate goals? California is a global climate leader, but we are dangerously at risk of not only falling short – but well short – of our emissions targets. It is not hyperbole to say that GGRF, deployed the right way, and in combination with existing programs including cap-and-invest, the RPS, and others, could be the difference between success or failure.

This blog simply summarizes over a decade of public data on GGRF – which unequivocally shows that programs including high-speed rail, affordable housing and sustainable communities, and transit, are extremely cost-ineffective and not even aligned with the state's main climate plan. We acknowledge that there are other benefits that can be derived from GGRF spending as opposed to purely emissions reductions (although, it is called the 'Greenhouse Gas Reduction Fund'). That said, a lot of the co-benefits, such as job creation and air quality improvements, could equally be achieved, and possibly bettered, by pivoting to economic opportunities that are also consistent with the state's climate goals.

Adopting an updated cap-and-invest program without delay is a priority to prevent any further uncertainty that is contributing to depressed allowance prices. If this can be paired with structural GGRF reform, policymakers can turn a difficult moment into a meaningful course-correction. Without this, we should not be surprised if California's cap-and-invest program is again exposed in future years.

* * *

[1] This assumes $13.1B in funding by 2030, as per California HSR 2024 Business Plan (p. 54): https://hsr.ca.gov/wp-content/uploads/2024/05/2024-Business-Plan-FINAL.pdf.

[2] This also assumes HSR achieves its forecast rider estimates, which determines the emissions reduction estimate. For more information, including the two scenarios considered by HSR Authority, see HSR 2023 Sustainability Report (p. 59): https://hsr.ca.gov/wp-content/uploads/2024/09/Sustainability-Report-2024-FINAL-A11Y-20240916.pdf.

[3] For more information on individual projects, see the CCI Detailed Dataset: https://www.caclimateinvestments.ca.gov/annual-report.